in All-Cash Deal, Co-Founded in 1996 by Robert Kelly")

in All-Cash Deal, AtaiBeckley Formed in 2025 from Merger of atai Life Sciences & Beckley Psytech, AtaiBeckley Current Market Value at $2.6 Billion, Share Price +84.8% YTD, +156.4% Last 12 Months & -58.8% Last 5 Years")

in APAC – Osaka, Seoul, Macau, Taipei, Mumbai, Top 5 Preferred Luxury Shopping Destinations for China HNWs – Hong Kong, France, United States, Japan, Europe (ex-UK, France, Italy), Top 5 Core Luxury Retail Destinations Price Per Sqm (Per Year) – London (Bond Street) $22,100, Hong Kong (Tsim Sha Tsui) $18,500, Milan (Via Monte Napoleone) $18,400, Los Angeles (Rodeo Drive) $15,100, Paris (Champs Elysées) $13,800, Top 5 New Luxury Store Openings by Cities in 2025 – New York, Beijing, Paris, Bangkok, Milan")

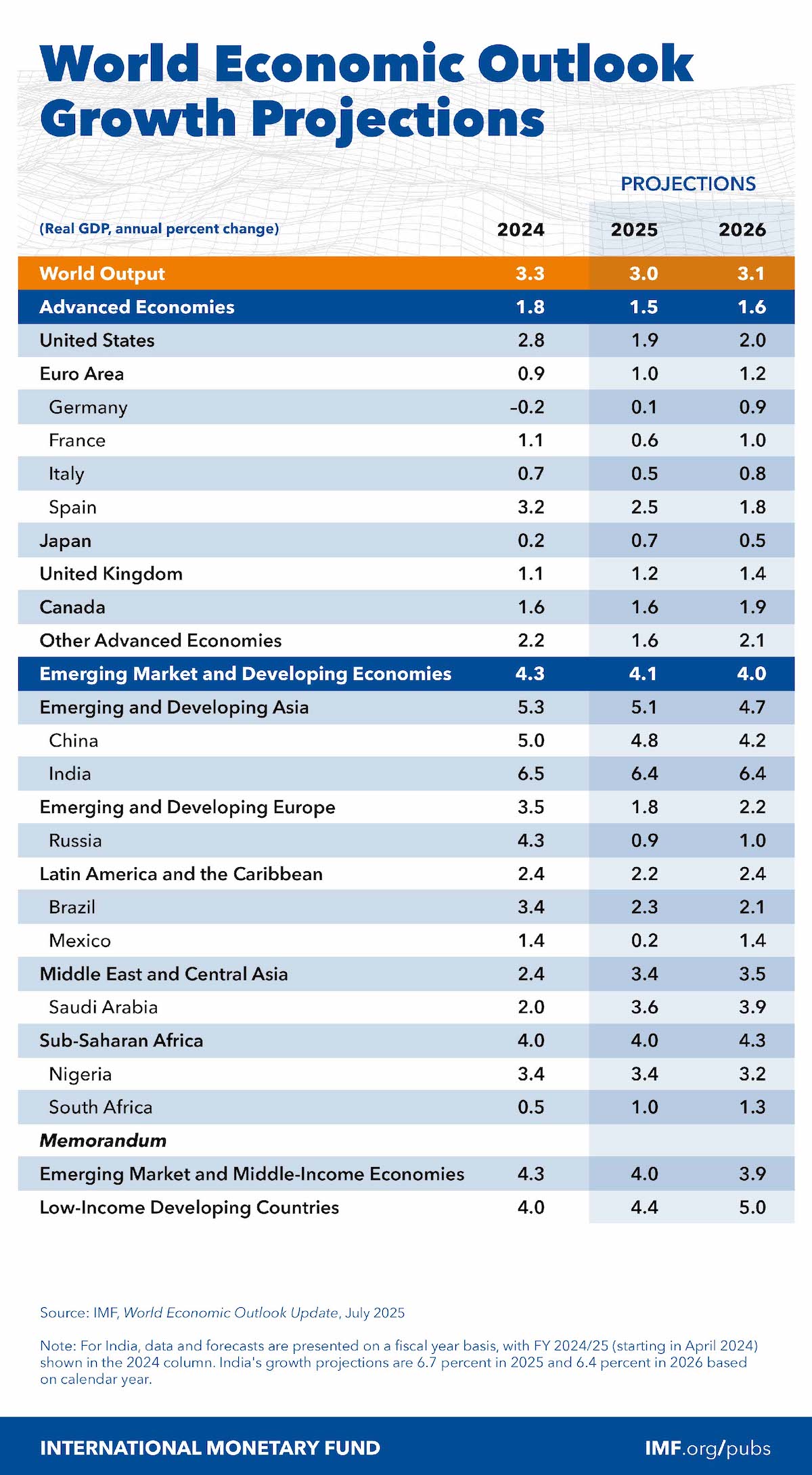

IMF World Economic Outlook 2025: Global GDP to Grow +3.1% with +3.6% Inflation in 2026, United States +2%, UK +1.4%, China +4.2%, India +6.4%, Japan +0.5%, Hong Kong +1.9% & Singapore +1.9% in 2026, 2025 Global Outlook – 1) Uncertainty Remained Elevated, 2) Global Inflation Mixed Signs, 3) US Effective Tariff Rate Underlying Projections 17.3%, 4) Prices for Energy Commodities Expected to Fall 7%, 5) Monetary Policy Rates in US & UK to Decline in 2025 2H, 6) Fiscal Stimulus Anticipated in Major Economies, 7) Global Growth Expected to Decelerate, 8) Upward Revision for 2025 is Broad Based, 9) Risks to Outlook Remain Tilted to Downside

21st August | Hong Kong

The International Monetary Fund (IMF) has released the IMF World Economic Outlook 2025 (July Update), providing key insights into global economy & GDP growth in 2025 & 2026. In 2026, Global GDP to grow +3.1% with +2.6% inflation, with United States +2%, UK +1.4%, China +4.2%, India +6.4%, Japan +0.5%, Hong Kong +1.9% & Singapore +1.9% in 2026. 2025 Global Outlook – 1) Uncertainty remained elevated, 2) Global inflation mixed signs, 3) US effective tariff rate underlying projections 17.3%, 4) Prices for energy commodities expected to fall 7%, 5) Monetary policy rates in US & UK to decline in 2025 2H, 6) Fiscal stimulus anticipated in major economies, 7) Global growth expected to decelerate, 8) Upward revision for 2025 is broad based, 9) Risks to outlook remain tilted to downside. See below for key findings & summary | View report here

“ IMF World Economic Outlook 2025: Global GDP to Grow +3.1% with +3.6% Inflation in 2026, United States +2%, UK +1.4%, China +4.2%, India +6.4%, Japan +0.5%, Hong Kong +1.9% & Singapore +1.9% in 2026, 2025 Global Outlook – 1) Uncertainty Remained Elevated, 2) Global Inflation Mixed Signs, 3) US Effective Tariff Rate Underlying Projections 17.3%, 4) Prices for Energy Commodities Expected to Fall 7%, 5) Monetary Policy Rates in US & UK to Decline in 2025 2H, 6) Fiscal Stimulus Anticipated in Major Economies, 7) Global Growth Expected to Decelerate, 8) Upward Revision for 2025 is Broad Based, 9) Risks to Outlook Remain Tilted to Downside “

The International Monetary Fund (IMF) has released the IMF World Economic Outlook 2025 (July Update), providing key insights into global economy & GDP growth in 2025 & 2026. See below for key findings & summary | View report here

IMF World Economic Outlook 2025 (July Update)

1) GDP Forecast:

GDP Growth Forecast (2025 / 2026):

- Global: +3% / +3.1%

- Advanced Economies: +1.5% / +1.6%

- Emerging Market and Developing Economies: +4.1% / +4%

Global Inflation Forecast (2025 / 2026): +4.2% / +3.6%

2025 / 2026 GDP Growth forecast in Americas:

- United States: +1.9% / +2%

- Canada: +1.6 / +1.9%

- Brazil: +2.3% / +2.1%

- Mexico: +0.2% / +1.4%

2025 / 2026 GDP Growth forecast in Europe:

- United Kingdom: +1.2% / +1.4%

- Germany: +0.1% / +0.9%

- France: +0.6% / +1%

- Italy: +0.5% / +0.8%

- Spain: +2.5% / +1.8%

- Netherlands: +1.2% / +1.2%

- Switzerland*: +0.9% / +1.6%

- Russia: +0.9% / +1%

2025 April Update*

2025 / 2026 GDP Growth Forecast in APAC:

- China: +4.8% / +4.2%

- India: +6.4% / +6.4%

- Japan: +0.7% / +0.5%.

- South Korea: +0.8% / +1.8%

- Taiwan*: +2.9% / +2.5%

- Hong Kong*: +1.5% / +1.9%

- Singapore*: +2% / +1.9%

- Indonesia: +4.8% / +4.8%

- Malaysia: +4.5% / +4%

- Thailand: +2% / +1.7%

- Philippines: +5.5% / +5.9%

- Vietnam*: +5.2% / +4%

- Australia: +1.8% / +2.2%

- New Zealand*: +1.4% / +2.7%

2025 April Update*

2025 / 2026 GDP Growth Forecast in Middle East:

- UAE*: +4% / +5%

- Saudi Arabia: +3.6% / +3.9%

- Israel*: +3.2% / +3.6%

- Egypt: +4% / +4.1%

- Iran: +0.6% / +1.1%

- Iraq*: -1.5% / +1.4%

- Qatar*: +2.4% / +5.6%

- Kuwait: +1.9% / +3.1%

2025 April Update*

Top 10 Economies in the World (GDP):

- United States – $29.1 trillion

- China – $18.7 trillion

- Germany – $4.6 trillion

- Japan – $4 trillion

- India – $3.9 trillion

- United Kingdom – $3.6 trillion

- France – $3.1 trillion

- Italy – $2.3 trillion

- Canada – $2.2 trillion

- Brazil – $2.1 trilion

Top 15 Economies in Asia-Pacific (GDP):

- China – $18.7 trillion

- Japan – $4 trillion

- India – $3.9 trillion

- Australia – $1.7 trillion

- South Korea – $1.7 trillion

- Indonesia – $1.3 trillion

- Taiwan – $782 billion

- Singapore – $547 billion

- Thailand – $526 billion

- Vietnam – $476 billion

- Philippines – $461 billion

- Bangladesh – $450 billion

- Malaysia – $421 billion

- Hong Kong – $407 billion

- Pakistan – $373 billion

Source (GDP): World Bank

2) 2025 Global Economy

- Global GDP – To increase to +3% in 2025, and +3.1% in 2026

- Global inflation – To decrease to +4.2% in 2025, and +3.6% in 2026

3) 2025 Global Outlook – July

A) Global Outlook – July Update

- Uncertainty remained elevated even as effective tariff rates have come down

- Global financial conditions have eased, US equity markets have largely rebounded, global equity markets have also rallied, US dollar depreciated further, defying expectations that tariffs and larger fiscal deficits would cause the currency to appreciate.

- Global trade grew robustly Q1, but high-frequency indicators point an unwinding of front-loading in Q2

- Global inflation showing mixed signs. The global median of sequential headline inflation has increased a notch, but core inflation has eased considerably and is now below 2%.

- US effective tariff rate underlying projections is 17.3%, compared with 24.4% in the April reference forecast. The corresponding effective tariff rate for the rest of the world is 3.5%, compared with 4.1% in the April reference forecast.

- Prices for energy commodities expected to fall by about 7% in 2025,

- Monetary policy rates in the United Kingdom and the United States expected to decline in the second half of 2025

- Fiscal stimulus anticipated in major economies in the near term, including China, Germany, and the United States.

- Global growth expected to decelerate, with apparent resilience due to trade-related distortions waning.

- The upward revision for 2025 is quite broad based, because it owes in large part to strong front-loading in international trade as well as to a lower worldwide effective tariff rate than assumed in the April reference forecast and to an improvement in global financial conditions.

- Global inflation is expected to continue to decline, with headline inflation falling to 4.2% in 2025 and 3.6% in 2026. This is virtually unchanged from the April WEO (World Economic Outlook), with trends of cooling demand and falling energy prices remaining in place.

- Overall, risks to the outlook remain tilted to the downside.

B) Policies recommendations / priorities:

- Countries should reduce policy-induced uncertainty by promoting clear & transparent trade frameworks. Pragmatic cooperation is paramount in instances in which some rules of the international trading system, in their current form, may not be functioning as intended.

- Restoring fiscal space and ensuring sustainable public debt is crucial, even while addressing critical spending needs. This requires credible medium-term fiscal consolidation with growth- friendly adjustments and a focus on rebuilding buffers. Countries should enhance fiscal revenues, improve spending efficiency, crowd in private sector investment, and use automatic stabilizers for negative demand shocks.

- Central banks must carefully calibrate monetary policies to country-specific circumstances to maintain price and financial stability amid prolonged trade tensions and evolving tariffs.

- The differing economic impact of tariffs across countries could complicate the trade-offs by introducing a divergence in monetary policy stances. Under normal circumstances, exchange rates should be allowed to adjust. The IMF’s Integrated Policy Framework provides guidance tailored to country-specific conditions on appropriate policy responses if disruptive movements in foreign exchange and risk premiums take hold.

- Ultimately, lifting medium-term growth prospects is the only sustainable way to ease macroeconomic trade-offs. Enduring structural reforms in areas such as labor markets, education, regulation, and competition can boost productivity, potential growth, and job creation. In addition, measures fostering technological advancements, including digitalization and the adoption of artificial intelligence, can further enhance productivity and potential growth.

4) 2025 April Update (Previous)

A) 2025 Global Outlook – April Update

- Global economy at critical juncture

- Major policy shifts are resetting the global trade system and giving rise to uncertainty

- United States tariffs against trading partners which have invoked countermeasures.

- Signs of stabilization were emerging through much of 2024 after a prolonged and challenging period of unprecedented shocks

- Inflation down from multi-decade highs followed a gradual though bumpy decline toward central bank targets

- Labor markets normalized with unemployment and vacancy rates returning to pre-pandemic levels

- Growth hovered around 3% in the past few years and global output came close to potential

- Diminished Policy Space – Much of the available policy space has already been exhausted in many countries, limiting how much support policymakers can give economies in case of new negative shocks or a pronounced downturn. Many countries passed large fiscal support packages, first during the pandemic and then as energy and food prices spiked at the onset of Russia’s invasion of Ukraine.

- High Public Debt amid Elevated Interest Rates – Fiscal space is now much tighter than a decade ago, and the fiscal adjustment required to stabilize debt ratios is at a historic high. At the same time, debt service as a fraction of fiscal revenue is rising Servicing costs remain below pandemic levels in countries where debt was incurred under favorable conditions during COVID-19, effective rates are likely to surpass prepandemic levels as debt rolls over, notably those for low-income countries and some emerging market and developing economies.

- Global Imbalances Arising from Domestic Imbalances – Rising geopolitical tensions and widening domestic imbalances, in particular, weak demand in China and strong demand in the United States – have renewed concerns about global imbalances. Since 2016–17, China and the United States have diversified their bases of trading partners, decoupling from each other in terms of export and import linkages

Assumptions:

- Monetary policy – In the United States, the federal funds rate is projected to be down to 4% at the end of 2025 and reach its long-term equilibrium of 2.9% at the end of 2028. In the euro area, 100 basis points in cuts are expected in 2025 (with three cuts having already occurred this year), representing two more 25 basis point cuts than in the assumptions underlying the October 2024 WEO, bringing the policy rate to 2% by the middle of the year. In Japan, policy rates are expected to be lifted at a similar pace as assumed in October 2024, gradually rising over the medium term toward a neutral setting of about 1.5%

- Fiscal policy – Governments in advanced economies on average are expected to tighten fiscal policy in 2025, 2026 and, to a lesser extent, in 2027.

- Commodity price – Prices of fuel commodities are projected to decrease in 2025 by 7.9%, with a 15.5% decline in oil prices and a 15.8% drop in coal prices offset by a 22.8% increase in natural gas prices

B) 4 Growth Upside

- Next-generation trade agreements

- Mitigation of conflicts

- Structural reform momentum

- Growth engine powered by artificial intelligence (AI)

C) 5 Downside Risks

- Escalating trade measures & prolonged trade policy uncertainty

- Rising long-term interest rates

- Rising social discontent

- Increasing challenges to international cooperation

- Labor supply gaps

D) 10 Central Bank policies recommendations / priorities:

- Delivering a stable and predictable trade environment

- Preserve international cooperation

- Calibrate monetary policy amid two-sided risk

- Safeguard financial stability through prudential policy

- Devise adjustment plans to restore fiscal sustainability

- Enact targeted fiscal reforms

- Protect growth & the vulnerable

- Use timely, targeted, temporary support where essential, in a responsible way

- Enact structural reforms for medium-term growth

- Make progress on climate policies

5) IMF World Economic Outlook 2025 Forecast – July Update

Caproasia Users

- Manage $20 million to $30 billion of assets

- Invest $3 million to $300 million

- Advise institutions, billionaires, UHNWs & HNWs

Caproasia Platforms | 11,000 Investors & Advisors

- Caproasia.com

- Caproasia Access

- Caproasia Events

- The Financial Centre | Find Services

- Membership

- Family Office Circle

- Professional Investor Circle

- Investor Relations Network

Monthly Roundtable & Networking

Family Office Programs

The 2026 Investment Day

- March - Hong Kong

- March - Singapore

- April - Hong Kong

- April - Singapore

- July - Hong Kong

- July - Singapore

- Sept- Hong Kong

- Sept - Singapore

- Oct- Hong Kong

- Nov - Singapore

- Visit: The Investment Day | Register: Click here

Caproasia Summits

- The Institutional Investor Summit

- The Investment / Alternatives Summit

- The Private Wealth Summit

- The Family Office Summit

- The CEO & Entrepreneur Summit

- The Capital Markets Summit

- The ESG / Sustainable Investment Summit

in All-Cash Deal, Co-Founded in 1996 by Robert Kelly")

in All-Cash Deal, AtaiBeckley Formed in 2025 from Merger of atai Life Sciences & Beckley Psytech, AtaiBeckley Current Market Value at $2.6 Billion, Share Price +84.8% YTD, +156.4% Last 12 Months & -58.8% Last 5 Years")

in All-Cash Deal, Representing +73% Premium to Unaffected Closing Price (15/7/26), Rotork Founded in 1957 by Jeremy & David Fry, Rotork Current Market Value at $5.3 Billion, Share Price +49.3% YTD, +49.2% Last 12 Months & +38.2% Last 5 Years")

in First Funding Round at $52 Billion Valuation in 2026 June, DeepSeek AI Model Built with $6 Million Funding, Founded in 2023 & Invested Solely by China $14 Billion Quant Hedge Fund High-Flyer Quant, DeepSeek CEO Liang Wenfeng is High-Flyer Quant Co-Founder, High-Flyer Quant Founded in 2015 Relying on Mathematics & AI for Quantitative Investment")

Protect Consumers, Younger & Vulnerable People, 2) Defend Integrity of Domestic Market & 3) Eliminate Money Laundering Vulnerabilities in Football Clubs & Agents (Flagged in UK National Risk Assessment)")

Reports $8.9 Billion (HKD 69.7 Billion) AUM & +14% Net IRR for 2025, Portfolio Geography: China Mainland 47%, Hong Kong 28%, Others 25%, Sector: Hard & Core Technology 56%, Biotech 22%, New Energy / Green Technology 9%, Others 13%, Investment Stage: Early 9%, Growth 58%, Mature 33%")

for 63 Children (Age 18 to 25) of UOB Privilege Banking Clients in Partnership with Singapore Management University (SMU) Business Families Institute & Steward Leadership Institute (SLI), UOB Privilege Banking Requires Minimum $270,000 (S$350,000) AUM")

in All-Cash Deal, Co-Founded in 1996 by Robert Kelly")